The de facto standard in asset management is the famous 60/40 (60% US stocks, 40% US bonds). And this is the standard we also use to benchmark our strategies and portfolios. Now, to question the use of the 60/40 ‘buy-and-hold’ strategy as not being the most appropriate benchmark for a tactical portfolio is completely justified. So why do we still use it as our default benchmark?

Should our sole aim be to maximise returns, we would have to look into speculative investment instruments like hedge funds or crypto. Returns can be stellar…, and are often followed by precipitous price drops. Even the most established crypto currency Bitcoin is subject to 75% drawdowns every few years. Saying “I would have traded that” in hindsight is easier than holding a position in real-time when the future is unknown. Are you willing to hold through wild swings and major losses or, like most retail investors, are you prone to buying high and selling low and therefore at risk whipping out hard earned capital?

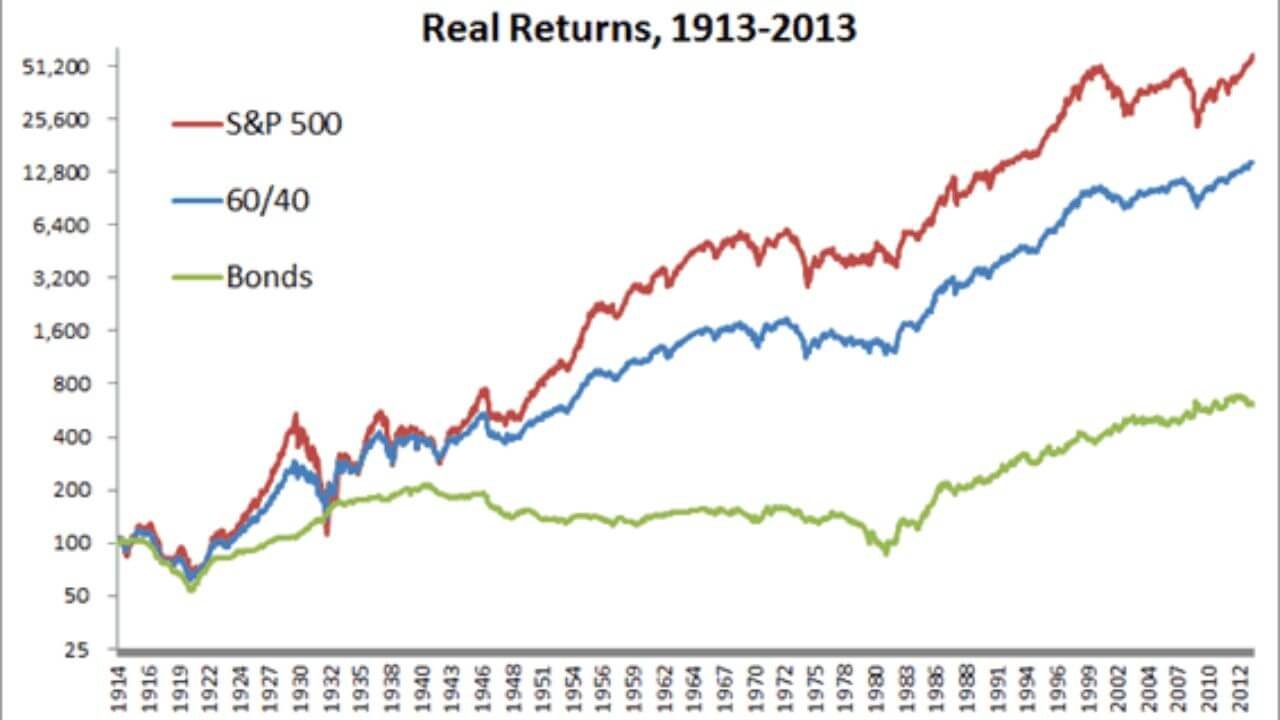

Our strategies and portfolios are not designed to only maximising returns but maximising returns relative to risk. Measures of risk-adjusted return include Sharpe Ratio, Sortino Ratio, and the Ulcer Performance Index, a measure of downward volatility, the amount of drawdown or retracement over a period. For example: the S&P-500 has outperformed a 60/40 holding by a little over 1% per year. At the same time, the S&P-500 exhibited 50% higher volatility and a 70% larger maximum drawdown. Therefore, on a risk-adjusted basis, the S&P-500 has been inferior. Comparing performance to a stock market index (or any other single undiversified asset for that matter) goes against that basic ethos.

Our point is that whatever the most appropriate benchmark is, it will always be a diversified portfolio and not a stock market index like the S&P-500. The 60/40 is the de facto standard in the asset management industry that has been a tough hurdle to beat over the last 40+ years.